Bordered by three continents and twenty two countries it is easy to understand why so many people choose to cruise around the Med’s hotspots. However, there is one thorny issue that I am sure everyone would agree can burst the so called ‘happy bubble’; clarity of regulatory requirements and in particular that dreaded word….VAT.

Notwithstanding the fact that yacht builders, owners, managers and brokers are having to continuously deal with the exact implications of the ever developing Maritime Laws, there is also a plethora of VAT rules adding to the bureaucratic maze in the EU.

One solution which effectively and efficiently deals with the EU VAT headache is the Malta VAT leasing scheme.

Why is VAT so important?

Yachts owned by EU resident individuals or corporate entities have the right to free movement throughout the EU provided VAT has been paid on the craft in one of the EU countries.

Yacht owners, irrespective of whether they are navigating in territorial waters of EU member states or sailing between EU countries, must carry evidence at all times that VAT has been paid or, if applicable, evidence that an exemption is applicable. Without such evidence there is the possibility that the yacht will be impounded and held by Customs.

How does VAT work?

For the uninitiated, VAT is a consumption tax charged on goods and services. When someone buys a yacht in the EU there is a requirement to pay VAT on that purchase thereby increasing the actual price of the yacht by a significant amount. The VAT amount due varies depending on the VAT rate applicable in the relevant EU Member State. EU VAT rates start at 17% going up to a whopping 27%.

However, depending on whether the customer purchasing the yacht is a private individual or a corporate entity affects the mechanism for charging the VAT element.

If the customer is a private individual then VAT at the rate applicable in the yacht builder’s EU country of establishment would be applied. The individual would have to pay the VAT and this would be an absolute cost to the individual.

Taxable person

However, if the customer purchasing the yacht is a corporate entity established in another EU Member State then the VAT rate applicable in the customers EU country can be charged.

Confusing isn’t it! Let’s look at the example below to explain in more detail:

A yacht builder in Italy sells a yacht to a Maltese registered company. The Maltese company is registered for VAT in Malta and so it provides the yacht builder with its Malta VAT number. The Italian yacht builder raises its sales invoice, including details of the Malta VAT number, and doesn’t charge Italian VAT on the sale of the yacht as the sale is considered to be a zero-rated EC supply. The Malta Company takes delivery of the yacht in Malta and records the purchase in its Malta VAT return as an EC Acquisition. The Malta Company has to charge itself the Malta standard rate of VAT on the EC Acquisition (currently 18%).

On the basis that the Maltese company is registered and trading as a shipping company it is considered to be carrying on an economic activity for VAT purposes and therefore such taxable activity means the business will be entitled to recover the VAT it has charged itself on the EC Acquisition of the yacht. The overall result is that the company charges itself Malta VAT and reclaims said VAT in the same VAT return resulting in a nil net effect so no significant cash flow issues arising.

The concept of ‘economic activity’ is a very important point to remember as this is the crux of most VAT issues and the reason why the Malta leasing scheme works so well.

Malta VAT leasing scheme

There are several underlying VAT principles which, when taken together, form the basis of the Malta VAT yacht leasing arrangements.

A leasing agreement of a pleasure boat is an agreement whereby the lessor (in this case the Malta Company) contracts the use of the yacht to the lessee (person who leases the yacht) in return for payment.

As discussed already the leasing of a pleasure yacht to a third party would be considered to be an economic activity so the leasing company has the right to recover VAT (subject to usual VAT rules). It also means that VAT has to be charged to the lessee in respect of the lease payments and this is where the Malta VAT leasing arrangements kick in and things get interesting.

In addition, the Malta leasing scheme allows for the lessee to purchase the vessel from the Lessor Company at the end of the lease period. This is completely optional so the lessee doesn’t have to buy the yacht at all if they don’t want to. If the lessee does exercise the option to purchase this would be subject to the standard rate of VAT (currently 18%).

How is the leasing agreement treated for VAT purposes?

For VAT purposes, the long term lease of a yacht (i.e. leased for more than 90 days) is considered to be a supply of services. The supply of such services is subject to VAT according to the use of the vessel. This means that, providing the lessor is a Maltese registered company and as per the guidelines laid down by the Malta VAT Department, VAT is due only on the portion of the lease which takes place within EU territorial waters.

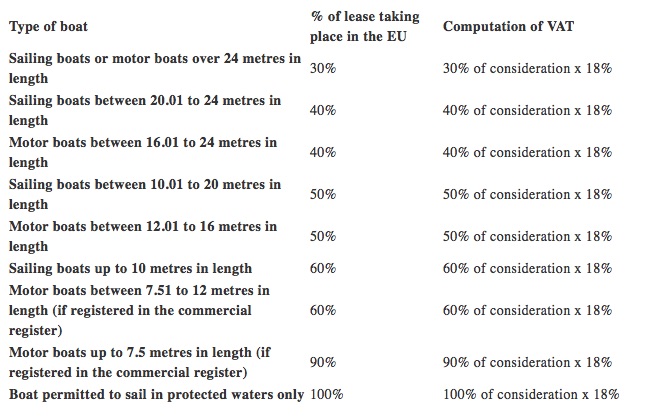

As it’s very difficult to track the movements of a yacht the Malta VAT Department has determined the following percentages to be the deemed amount of use of a yacht in EU territorial waters:

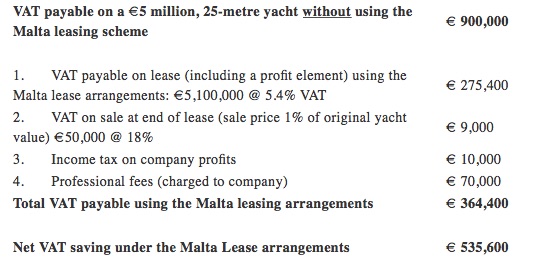

Taking the first type of craft as an example, a sailing yacht over 24 metres in length is presumed to sail in EU waters for 30% of the time during which it is leased. The VAT payable on the lease is charged ay the normal rate of VAT (18%) but only on 30% of the lease (i.e. presumed use in EU waters) which equates to 5.4% VAT due on the total value of the lease. For this example let’s presume the yacht is being purchased for €5 million:

There are a number of criteria which must be adhered to in order to successful apply the Malta VAT leasing arrangements. These are as follows:

1. The Lessor must be a company established in Malta. There are no restrictions in terms of who can be the lessee, it can be any Maltese or non-Maltese person or company.

2. Pre-approval to apply the Malta leasing arrangements is required from the VAT Department.

3. The lease can run for between 12 and 36 months, with monthly payments required. The lessor company must be seen to make a profit.

4. At the end of the lease period the lessee may opt to purchase the boat at a percentage of the original price. The final purchase is strictly an option which may be exercised at the end of the lease for a separate consideration. The consideration would be subject to Malta VAT at the full 18%.

5. The yacht must come to Malta at the start of the lease.

6. If the lessee exercises an option to purchase the boat after the end of the lease, a VAT paid certificate will be issued to the lessee provided that all VAT due has been paid.

Conclusion

The Malta VAT arrangements on yacht leasing are clearly not unique in the EU. France and Italy have had such an arrangement in place for a number of years and Malta’s system, when introduced in 2005 was modelled on the Italian system. More recently, Cyprus has also introduced an arrangement that reflects very closely Malta’s system.

The detailed implementation of the yacht leasing VAT arrangements are different in each of the above jurisdictions and the conditions imposed by the authorities are not identical. However, every country’s technical and legal basis for implementing the arrangement is invariably Article 58 of the VAT Directive.

It’s also worth pointing that although the Malta yacht leasing VAT arrangements have been in place since November 2005, the European Commission has never commenced any infringement procedures against Malta for an incorrect application of the VAT Directive. This attitude clearly contrasts with the rapid action taken by the Commission in cases where a Member State is clearly in breach of the VAT Directive’s dispositions, such as for example France’s abandoned interpretation of the VAT exemption on the chartering of pleasure yachts.

Written for Superyachtinvestor.com by:

Samantha Snow, Client Services Manager

samantha.snow@abacusmalta.com